There was a time when the word “blockchain” instantly made people think about Bitcoin, crypto millionaires, or internet speculation. Today, the conversation inside real businesses looks very different.

Executives are no longer asking, “What is blockchain?”

They’re asking:

- Can it reduce fraud?

- Can it improve supply chain visibility?

- Can it automate contracts?

- Can it protect customer data?

- Can it help us compete in a digital-first economy?

From logistics companies and healthcare providers to banks, manufacturers, and cloud-based SaaS businesses, blockchain is slowly moving from hype into practical business infrastructure.

And honestly, that shift was inevitable.

As someone with experience in business consulting, IT engineering, cloud computing, and enterprise systems, I’ve seen firsthand how companies struggle with one major issue: trust between systems, people, and organizations.

That’s exactly where blockchain starts becoming useful.

Not because it’s trendy.

Not because it’s connected to cryptocurrency.

But because modern businesses are drowning in disconnected data, inefficient workflows, compliance risks, and manual verification processes.

Blockchain solves part of that problem in a surprisingly elegant way.

The Real Meaning of Blockchain in Business

At its core, blockchain is simply a secure and shared digital ledger.

Think of it like a business record book that cannot easily be altered, manipulated, or secretly changed after information is recorded.

Instead of one company controlling the database, multiple participants share access to the same verified records.

That changes everything.

Traditional business systems usually rely on centralized control:

- One bank owns the transaction records

- One company controls inventory data

- One platform verifies identities

- One server stores contracts

Blockchain introduces a distributed approach where records are validated collectively instead of relying on a single authority. Researchers continue to highlight blockchain’s value in transparency, immutability, and decentralized trust systems. (ScienceDirect)

For businesses, this creates opportunities to improve:

- Transparency

- Security

- Auditability

- Automation

- Cross-company collaboration

- Digital trust

And in today’s economy, trust is becoming one of the most valuable business assets.

Why Businesses Are Paying Attention Now

A few years ago, blockchain projects were often experimental.

Today, businesses are approaching blockchain more strategically because several things changed at the same time:

1. Cloud Computing Made Adoption Easier

Companies no longer need to build blockchain infrastructure from scratch.

Major cloud providers now offer Blockchain-as-a-Service platforms that simplify deployment, hosting, integration, and scaling. (Wikipedia)

This lowered the barrier to entry dramatically.

A mid-sized company can now experiment with blockchain without hiring an entire research division.

2. Cybersecurity Risks Keep Growing

Data breaches are becoming more expensive every year.

Businesses are realizing that centralized systems create attractive targets for attackers. Blockchain’s distributed structure can reduce certain types of tampering and unauthorized modification risks.

It’s not a magical cybersecurity solution, but it can strengthen integrity and traceability in critical business processes.

3. Customers Want More Transparency

Modern consumers want proof.

They want to know:

- Where products come from

- Whether goods are authentic

- How data is used

- Whether sustainability claims are real

Blockchain gives companies a way to provide verifiable digital records instead of relying purely on marketing claims.

4. Smart Contracts Are Changing Operations

One of the most practical blockchain innovations is the smart contract.

A smart contract is essentially software that automatically executes agreements when conditions are met.

For example:

- Payment releases automatically after delivery confirmation

- Insurance claims process automatically

- Supplier approvals trigger instantly

- Royalties distribute without manual accounting

That means fewer delays, fewer intermediaries, and fewer administrative bottlenecks.

How Blockchain Is Actually Being Used in Business

One of the biggest misconceptions is that blockchain is only useful for finance or cryptocurrency.

In reality, some of the most interesting use cases are happening outside crypto.

Supply Chain Management

This is probably one of the strongest real-world business applications today.

Traditional supply chains are fragmented.

A single product might involve:

- Manufacturers

- Suppliers

- Shipping companies

- Warehouses

- Retailers

- Customs agencies

Each organization maintains separate records, which creates inconsistencies, delays, and disputes.

Blockchain allows everyone to work from a shared source of truth.

For example, businesses can track:

- Product origin

- Shipment history

- Storage conditions

- Authenticity verification

- Compliance records

That becomes especially valuable in industries like:

- Pharmaceuticals

- Food production

- Luxury goods

- Electronics

- Manufacturing

When a contamination issue or counterfeit problem occurs, companies can trace the source much faster.

Financial Services

Banks and financial institutions were among the earliest enterprise blockchain adopters.

Why?

Because traditional financial systems involve many intermediaries.

Cross-border payments, for example, can still take days because multiple institutions verify transactions manually.

Blockchain can streamline settlement processes while reducing operational friction.

Some financial institutions are also exploring:

- Tokenized assets

- Digital identity verification

- Fraud prevention

- Trade finance automation

- Real-time settlements

This doesn’t mean traditional banking disappears.

It means backend infrastructure becomes faster and more efficient.

Healthcare

Healthcare systems struggle with fragmented patient data.

Different hospitals, clinics, and providers often use disconnected systems.

Blockchain can help create secure patient records with controlled access permissions.

That could improve:

- Medical record portability

- Prescription verification

- Insurance processing

- Clinical trial transparency

- Data integrity

The healthcare industry still faces regulatory and privacy challenges, but the long-term potential is enormous.

Real Estate

Real estate transactions are often slow, paperwork-heavy, and filled with verification steps.

Blockchain could simplify:

- Property ownership records

- Smart leasing contracts

- Digital title transfers

- Escrow processes

- Transaction history verification

In some markets, tokenized real estate investments are also creating new ways for smaller investors to access property ownership opportunities.

Digital Identity and Authentication

Identity fraud is becoming a massive global issue.

Businesses spend huge amounts verifying users, customers, and transactions.

Blockchain-based identity systems can allow individuals to control their own credentials while enabling secure verification.

This could improve:

- KYC processes

- Online authentication

- Credential verification

- Employee onboarding

- Academic certification validation

Several blockchain governance and identity frameworks are actively being researched for enterprise applications. (arXiv)

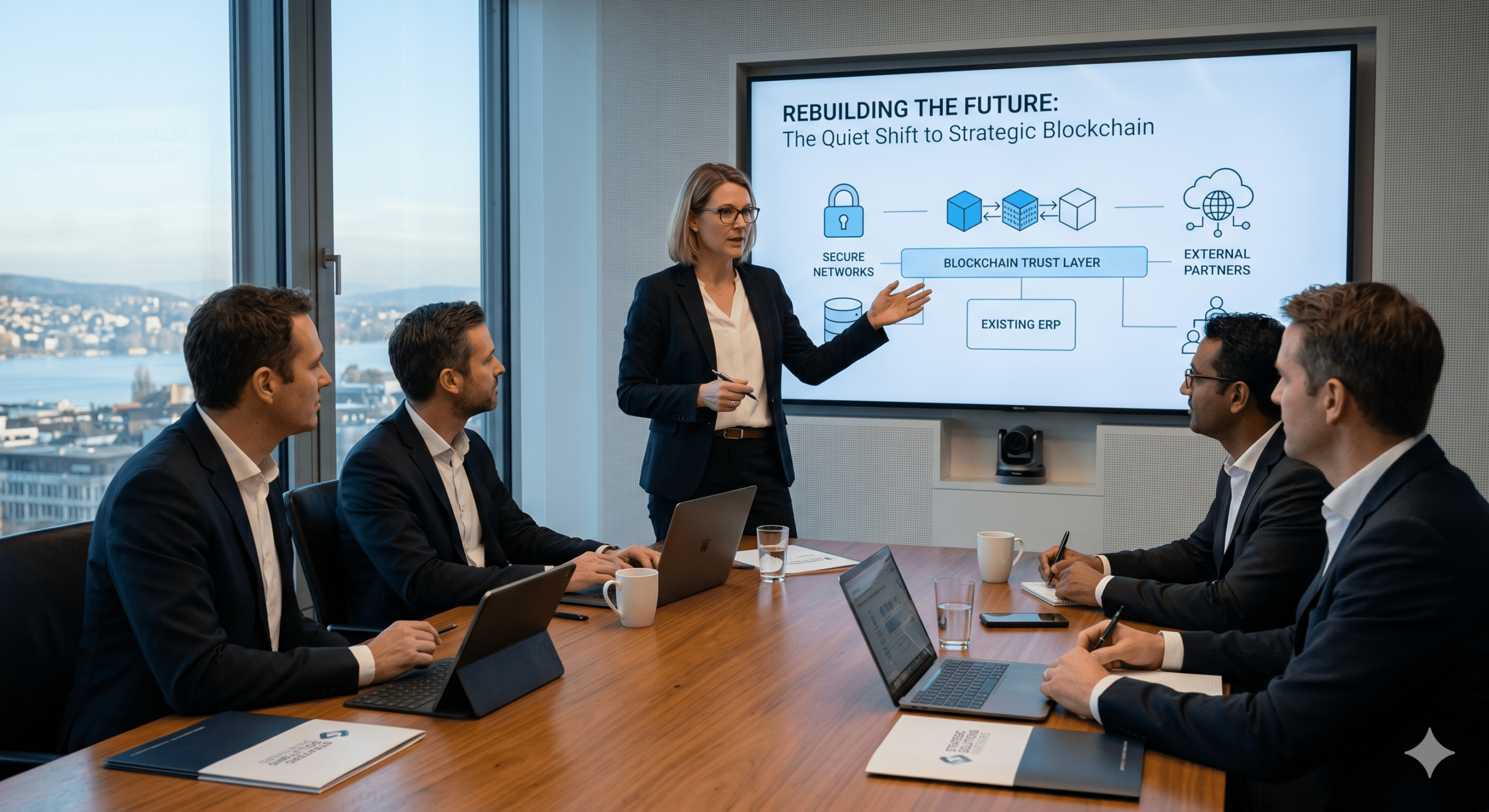

Blockchain and Cloud Computing: A Powerful Combination

This is where things get especially interesting from an IT and business strategy perspective.

Blockchain alone is not enough.

Cloud computing is what makes blockchain scalable for modern enterprises.

Cloud platforms provide:

- Elastic infrastructure

- Scalable storage

- Global availability

- API integrations

- Security tooling

- Analytics capabilities

Blockchain provides:

- Immutable records

- Distributed trust

- Transaction verification

- Shared transparency

Together, they create powerful enterprise ecosystems.

That’s why many businesses are moving toward hybrid architectures where cloud services handle scalability while blockchain manages verification and trust layers.

This is one reason Blockchain-as-a-Service continues to gain enterprise attention. (Wikipedia)

The Biggest Mistake Businesses Make About Blockchain

Many companies still approach blockchain backwards.

They start with the technology instead of the business problem.

That almost always fails.

Blockchain is not automatically better than traditional databases.

In fact, researchers continue to point out that blockchain should only be used when decentralized trust, transparency, and distributed verification are genuinely needed. (ScienceDirect)

A normal database is still better for many applications.

Businesses should ask:

- Do multiple parties need shared access?

- Is trust between organizations limited?

- Do records need immutability?

- Is auditability critical?

- Are intermediaries slowing operations?

If the answer is yes, blockchain may provide real value.

If not, traditional systems may be simpler and cheaper.

Good technology decisions are never about hype.

They’re about solving real operational problems.

Why Blockchain Adoption Still Feels Slow

Despite all the excitement, blockchain adoption remains gradual for several reasons.

Regulatory Uncertainty

Governments worldwide are still developing regulations around digital assets, decentralized systems, and blockchain governance.

Businesses hesitate when compliance rules are unclear.

Integration Complexity

Most companies already operate legacy systems.

Integrating blockchain into existing ERP, CRM, accounting, or cloud environments can be difficult.

Skills Gap

There’s still a shortage of experienced blockchain architects and enterprise developers.

Many companies simply don’t have internal expertise yet.

Scalability Challenges

Some blockchain networks still struggle with speed and transaction volume.

Enterprise-grade performance continues improving, but limitations remain in certain implementations.

Misunderstanding the Technology

This is probably the biggest issue.

Too many executives still associate blockchain only with speculation or cryptocurrency volatility.

That prevents them from seeing legitimate enterprise use cases.

The Rise of Tokenization in Business

One of the fastest-growing business trends is tokenization.

Tokenization means converting ownership rights or assets into digital blockchain-based tokens.

This could apply to:

- Real estate

- Art

- Stocks

- Loyalty rewards

- Intellectual property

- Event tickets

- Supply chain assets

For businesses, tokenization creates new opportunities for:

- Fractional ownership

- Faster transfers

- Digital marketplaces

- Liquidity

- Automated compliance

This trend is still evolving, but it has the potential to reshape how businesses manage ownership and transactions.

Blockchain Governance Matters More Than Technology

One lesson many organizations learn quickly is that blockchain success depends heavily on governance.

Who controls permissions?

Who validates transactions?

How are disputes resolved?

How are upgrades approved?

These governance questions become critical in enterprise environments. Researchers studying blockchain governance frameworks emphasize accountability, decentralization balance, and decision-making structures as major success factors. (arXiv)

Without proper governance, blockchain projects can become chaotic very quickly.

Technology alone is never enough.

Business processes, leadership alignment, legal compliance, and operational clarity matter just as much.

Will Blockchain Replace Traditional Business Systems?

No.

And that’s an important reality check.

Blockchain is not replacing:

- Cloud databases

- ERP systems

- CRM platforms

- Accounting software

- Enterprise applications

Instead, blockchain is becoming another layer inside modern digital ecosystems.

Think of it as a specialized trust infrastructure.

Businesses will continue using:

- Cloud platforms

- AI systems

- Data analytics

- APIs

- SaaS tools

Blockchain simply adds additional capabilities where transparency, verification, and decentralized coordination matter.

The future is integration, not replacement.

The Connection Between AI, Blockchain, and Business

One of the most exciting developments is how AI and blockchain may eventually work together.

AI is incredibly powerful at generating insights and automation.

But AI systems also raise concerns around:

- Data authenticity

- Trustworthiness

- Ownership

- Manipulation

- Verification

Blockchain can help create transparent audit trails for AI-generated processes and data usage.

In the future, businesses may use blockchain to verify:

- AI decision histories

- Training data provenance

- Automated contract execution

- Digital identity systems

- Intellectual property ownership

This intersection could become one of the most important enterprise technology trends of the next decade.

What Small Businesses Should Know About Blockchain

Many small business owners assume blockchain is only for giant corporations.

That’s no longer true.

Smaller businesses can already benefit from blockchain through:

- Payment systems

- Smart contracts

- Digital authentication

- Supply chain tracking

- Loyalty programs

- Document verification

The key is starting small.

Don’t build blockchain projects just to sound innovative.

Build them when they create measurable business value.

Sometimes the best first step is simply learning how the technology works and identifying inefficiencies inside existing workflows.

Industries Most Likely to Benefit Long-Term

Some industries are especially well-positioned for blockchain adoption.

Logistics and Supply Chain

Because transparency and tracking are critical.

Banking and Financial Services

Because transaction verification and settlement efficiency matter enormously.

Healthcare

Because secure records and data integrity are essential.

Manufacturing

Because global supplier coordination is complex.

Insurance

Because claims automation can reduce fraud and administrative costs.

Government Services

Because public records and identity verification require trust and transparency.

The Future of Blockchain in Business

We are probably entering the most practical phase of blockchain adoption.

The loud hype cycle is fading.

That’s actually a good thing.

The businesses succeeding with blockchain today are usually not the ones making the biggest headlines.

They’re the companies quietly improving operations behind the scenes.

They’re using blockchain to:

- Reduce friction

- Increase trust

- Improve visibility

- Strengthen security

- Automate workflows

- Modernize digital infrastructure

And honestly, that’s where real transformation happens.

Not in speculation.

Not in buzzwords.

But in solving everyday business problems more efficiently.

Final Thoughts

Blockchain is no longer just a futuristic experiment.

It’s becoming part of the larger digital transformation happening across industries worldwide.

Will every company need blockchain?

Probably not.

But businesses that understand where blockchain genuinely adds value will have an advantage as digital ecosystems become more connected, automated, and trust-driven.

The smartest organizations are approaching blockchain with balance.

They’re not blindly chasing trends.

They’re carefully identifying where transparency, automation, and decentralized trust can improve real business operations.

And from what I’ve seen across IT engineering, cloud infrastructure, and enterprise consulting, that practical mindset is exactly what separates successful digital transformation from expensive technology experiments.

The future of blockchain in business will not be built by hype.

It will be built by companies quietly solving real problems better than everyone else.

Further Reading From High-Authority Sources

- NIST Blockchain Technology Overview (arXiv)

- Blockchain as a Service Overview

- Harvard-Referenced Blockchain Business Research Topics

- Blockchain Governance Framework Research